Como fazer seu filho um filho de um filho para o seu filho para o seu filho para o seu filho, um filho de um milhão para o seu filho, um filho de um milhão para o seu filho, o que é um filho de um filho para o seu filho, o seu filho, que é um filho de um filho, para que o seu filho seja o seu filho para o seu filho, o que é um filho do seu filho para o seu filho, o que é um filho do seu filho para o seu filho, o que é um filho do seu filho para o seu filho, o que é um filho do seu filho para o seu filho, o que é um filho do seu filho para o seu filho, o que é um filho do seu filho para o seu filho, o seu filho, que é um filho do seu filho para o seu filho, o seu filho, que é um filho de um filho de um filho de um filho de um filho para o seu filho. Milionário! 💰👶

Learn how to turn just €62/month into a million for your child using smart investments, government subsidies, and tax strategies to make your child a millionaire! 💰👶

Teclações -chave

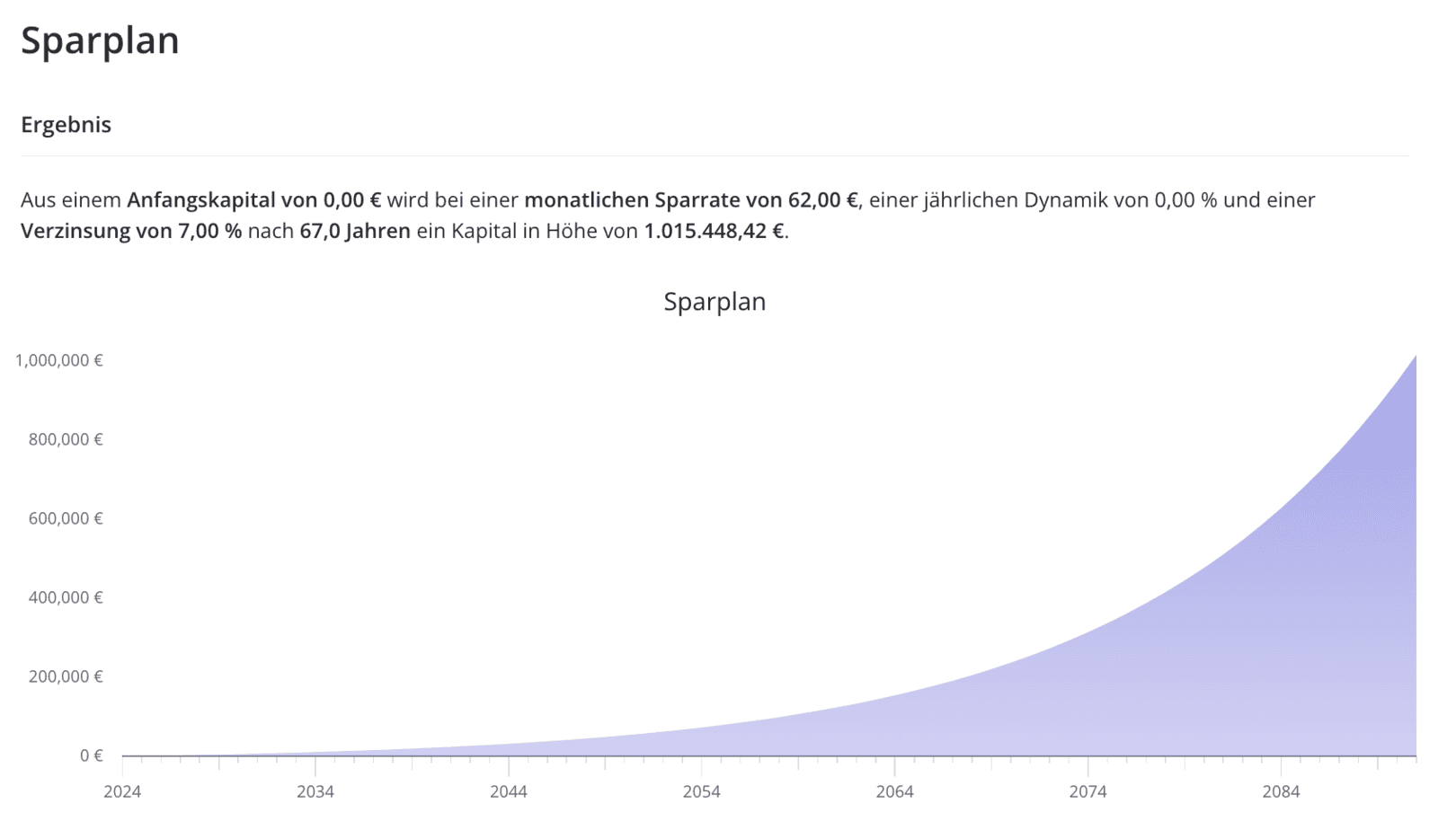

- Você pode fazer o seu Child A Millionaire com = € 62/mês || 123 , using government subsidies and investments.

- Raising kids is costly, but government subsidies Ajuda Reduce A carga financeira significativamente. Elterngeld apóia a criação de filhos nos primeiros anos.

- Mutterschaftsgeld ensures salary continuation during maternity leave; Elterngeld supports raising children in early years.

- Avoid savings accounts, insurance plans, and Bausparvertrag due to poor returns; melhores opções de investimento Existe para crescimento.

- Invest in ETFs, real estate, and precious metals to ensure long-term growth, stability, and financial security for your child’s future.

- Start early , invest smartly, and help secure a FUTURO FINANCEIRO PRONTEROUS para seu filho. Para acessar o conteúdo real, clique no botão abaixo. Observe que isso compartilhará dados com fornecedores de terceiros. Ao investir estrategicamente um modesto

You are currently viewing a placeholder content from YouTube . To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationIntroduction

Raising children is an expensive journey, but there’s a powerful way to give them a financial head start in life. By strategically investing a modest € 62 por mês , você pode tornar seu filho A Milionaire quando eles retirarem .

This method leverages government subsidies , tax savings e Interesse composto para garantir um futuro próspero para o seu filho. Neste artigo, percorreremos passo a passo como você pode conseguir isso sem precisar ser um especialista financeiro. De acordo com o

The High Cost of Raising Children in Germany

Raising a child in Germany is costly. According to the Escritório Estatístico Alemão , a criança média custa em torno de € 763 por mês , aumentando um impressionante € 165.000 Quando eles atingem a idade adulta. Este número é baseado em 2018 dados e, considerando o aumento dos custos de vida, provavelmente é muito mais alto hoje. De

Thankfully, German parents have access to numerous government subsidies to help ease the financial burden. From MUTTERSCHAFTSGELD TO Kindgeld , esses subsídios também podem ser estrategicamente = 195 = 191 = 191 to provide long-term benefits for your child’s financial future.

Government Benefits You Can Take Advantage Of

Several Government Benefícios estão disponíveis para ajudar os pais na Alemanha a gerenciar os custos da criação de filhos. O primeiro é MuttersChaftSgeld, que cobre o período de licença de maternidade - 6 semanas antes e 8 semanas após o nascimento . Este benefício, combinado com a contribuição do seu empregador, garante que o salário líquido permaneça intacto.

Next, Elterngeld supports parents who take time off work to care for their newborn, and Kindergeld provides at least €250 per month until your child turns 18 or even up to age 25. Parents can also claim KinderFreibetrag , um subsídio isento de impostos, que às vezes pode ser mais benéfico do que receber o Kindgeld. Estes Fundos e deduções fiscais podem ser usadas para impulsionar o futuro do seu filho investindo sabiamente. Para acessar o conteúdo real, clique no botão abaixo. Observe que isso compartilhará dados com provedores de terceiros. Se você investir o

You are currently viewing a placeholder content from YouTube . To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationThe Power of Compounding Interest

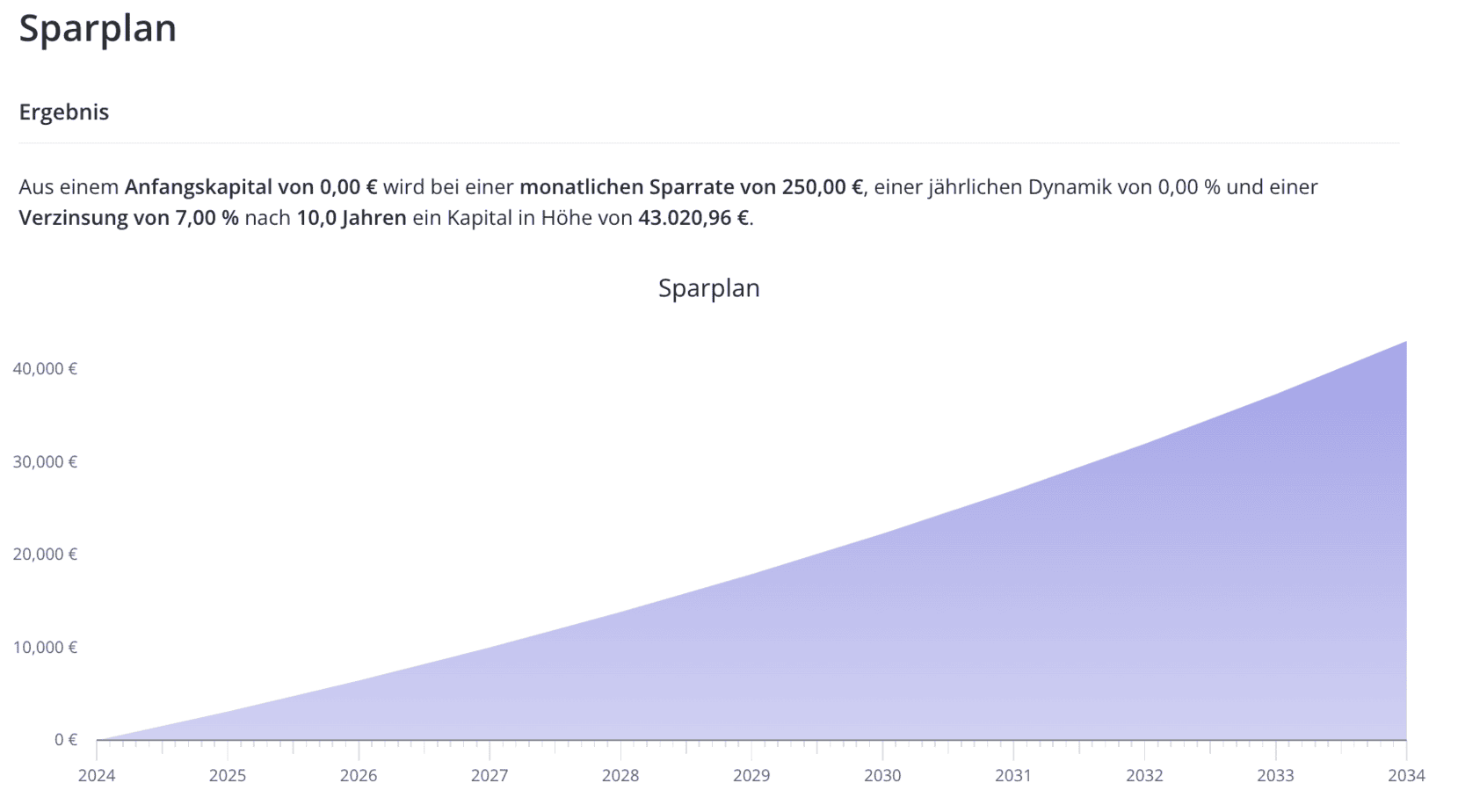

Compounding interest is one of the most powerful tools for growing wealth, especially when you start early. If you invest the € 250 Jardim de infância todos os meses para o seu filho, ele pode crescer para € 43.000 em apenas 10 anos.

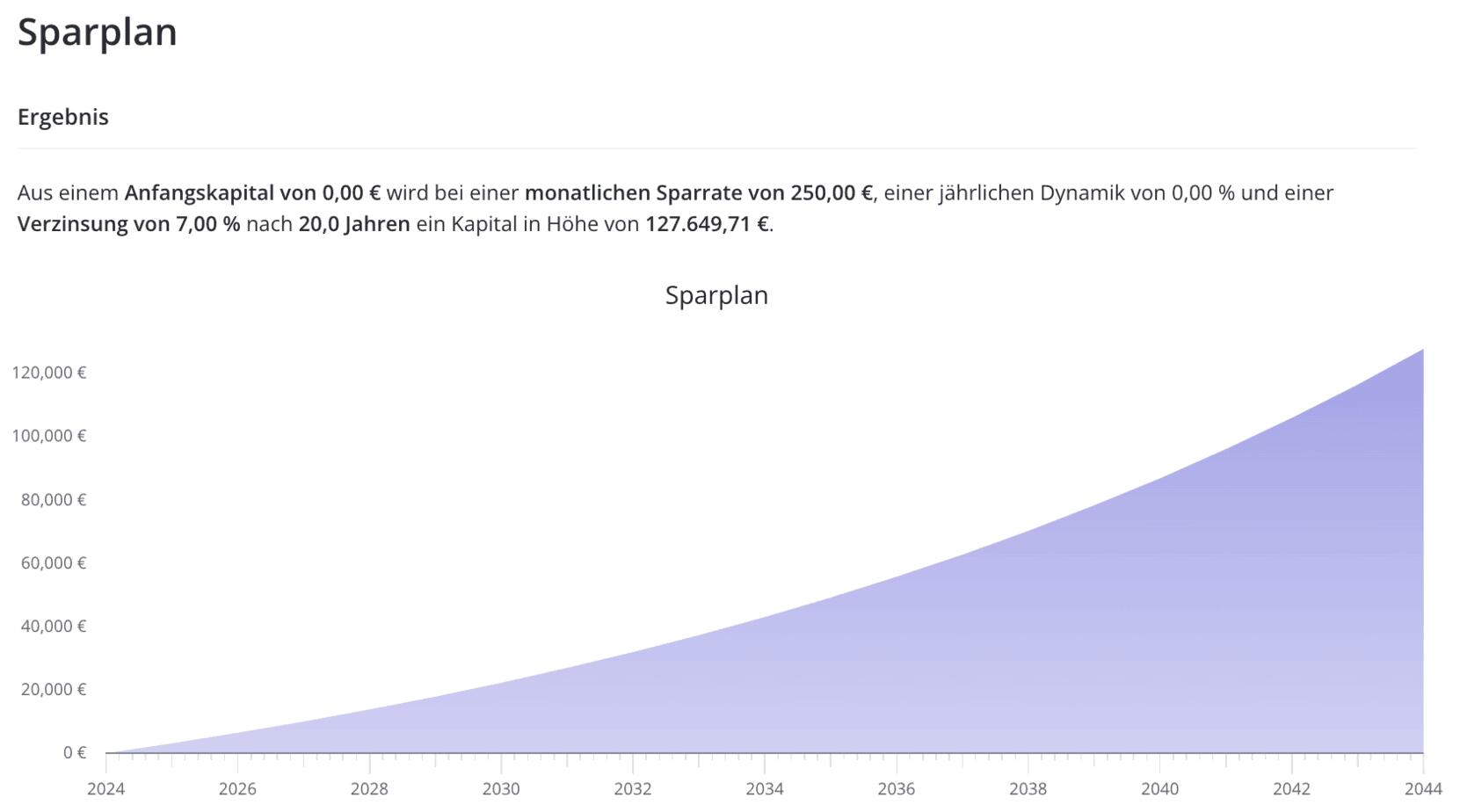

If you keep the investment going for 20 years , it could increase to almost € 130.000 . Imagine seu filho tendo uma soma tão grande para usar para sua primeira casa ou outros investimentos na vida. Quanto mais cedo você iniciar, mais tempo composto de tempo tiver que trabalhar sua mágica, transformando até pequenas contribuições em riqueza significativa. Muitos pais alemães ainda confiam

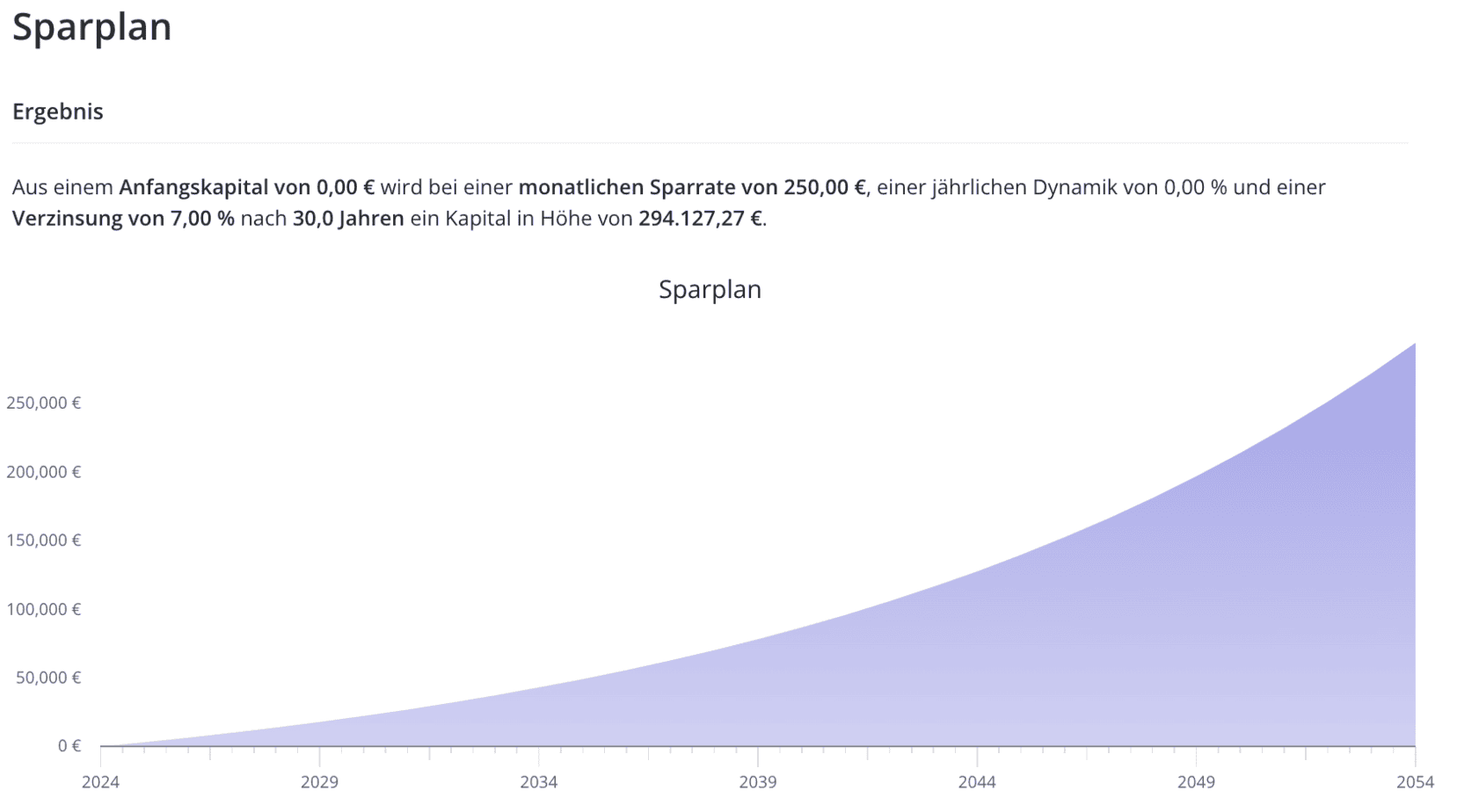

Keep it going for 30 years , and you’re looking at nearly €300,000 ! The earlier you start, the more time compound interest has to work its magic, turning even small contributions into significant wealth.

Investing Wisely: What to Avoid

Savings Accounts:

While investing is crucial, it’s just as important to know what to avoid. Many German parents still rely on Métodos de investimento desatualizado como Contas de poupança , que oferecem pouco ou nenhum interesse. As taxas de juros atuais significam que seu dinheiro está essencialmente apenas sentado lá, NÃO FAZER NADA . No entanto, quando se trata de crescimento a longo prazo, evitar contas de poupança e explorar melhores opções é essencial para maximizar os retornos para o futuro do seu filho. Esses produtos de seguro, como

This mindset stems from past experiences like the Telekom stock crash in the 90s, which left many Germans wary of riskier investments . However, when it comes to long-term growth, avoiding savings accounts and exploring better options is key to maximizing returns for your child’s future.

Why You Should Avoid Kid-Specific Insurance Plans

Germany offers various insurance plans designed for children, but they often don’t make financial sense. These insurance products, such as Ausbildungsversicherung , combinam economia com apólices de seguro como Seguro de invalidez . No entanto, os retornos são notoriamente baixos - geralmente tão pouco quanto 1,25% . Em vez disso, siga as opções de retorno mais alto, como o KidsPolice, ETFs, ou

When even a standard savings account can yield better returns, it’s clear that these insurance plans are a poor investment choice. Instead, stick with higher-return options like Kidspolice, ETFs, or imobiliário para proteger o futuro financeiro de seu filho.

The Pitfalls of Bausparvertrag

Another common investment mistake is the Bausparvertrag , which promises home-buying benefits but raramente entrega . Com uniformes Lower Retorna do que os planos de seguro específicos para crianças e rígidos Mortage Termos de retorno, o bausparvertrag é frequentemente um ponto de saída para o seu dinheiro. É uma ferramenta que não atende às necessidades financeiras modernas e você deve evitá -lo a todo custo.

Em vez disso, se imobiliário for seu objetivo, considere comprar uma propriedade diretamente. Você pode comprar um Propriedade pequena e pagar a hipoteca enquanto seu filho ainda é jovem. Quando eles são adultos, você pode presente ou herdar O imposto de imposto de propriedade, dando a eles um ativo valioso para iniciar sua vida. Para acessar o conteúdo real, clique no botão abaixo. Observe que isso compartilhará dados com provedores de terceiros. Para acessar o conteúdo real, clique no botão abaixo. Observe que isso compartilhará dados com provedores de terceiros. Para acessar o conteúdo real, clique no botão abaixo. Observe que isso compartilhará dados com provedores de terceiros. Fundos) estão entre as melhores opções de investimento para o crescimento da riqueza. Esses fundos são essencialmente cestas de vários estoques ou títulos que você pode comprar facilmente através de um

You are currently viewing a placeholder content from YouTube . To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from YouTube . To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationYou are currently viewing a placeholder content from YouTube . To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationInvesting Wisely: What to Get

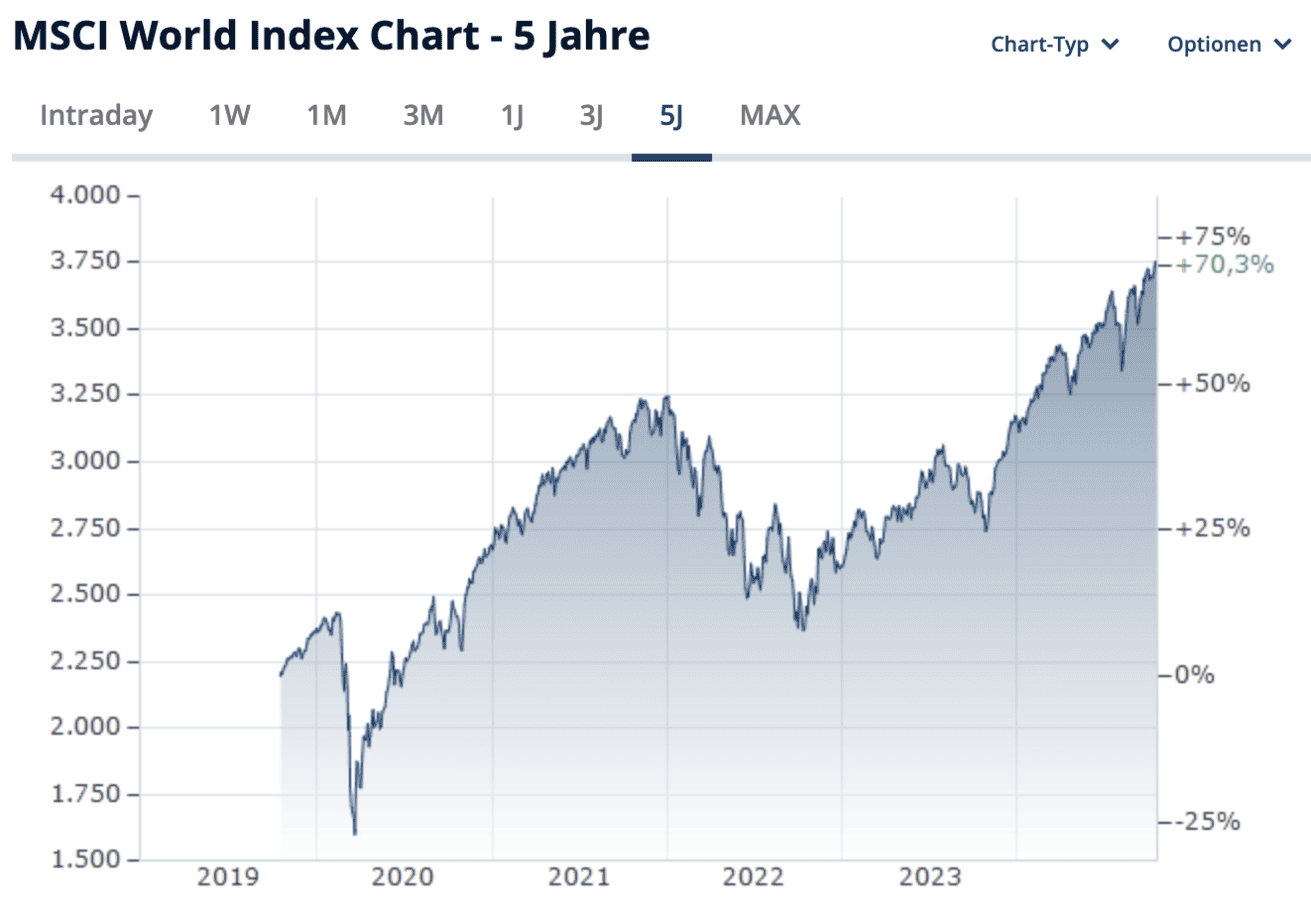

ETFs: The Modern Investment Solution

ETFs (Exchange Traded Funds) are among the best investment options for growing wealth. These funds are essentially baskets of various stocks or bonds that you can easily buy through a Corretagem ou um KidsPolice. Eles oferecem diversidade, simplicidade e retornos sólidos. Uma dica importante: a configuração de uma conta de corretora em nome do seu filho permite se beneficiar de ganhos de capital sem impostos de até

Investing in ETFs for your child provides long-term growth potential while minimizing risk. One important tip: setting up a brokerage account in your child’s name allows them to benefit from tax-free capital gains of up to € 1.000 anualmente .

However, there are tax implications and potential drawbacks, like your child gaining control of the account at 18 . Para obter mais controle e eficiência tributária, considere colocar ETFs em uma conta “ Pension ”, onde os fundos crescem sem impostos até você decidir liberá-los. Compra A

Real Estate: A Smart Long-Term Investment

Real estate can be one of the smartest investments you make for your child’s future. Buying a Propriedade pequena e pagar a hipoteca enquanto seu filho cresce significa que pode iniciar a idade adulta com uma casa paga e Receita passiva de aluguel . Além disso, desde que a propriedade seja avaliada em menos de

This strategy provides financial stability and opens doors to future opportunities. Plus, as long as the property is valued at less than € 400.000 , você pode presenteá-lo completamente ao seu filho isento de impostos . É um investimento que cresce em valor e oferece segurança a longo prazo. Nos últimos cinco anos, o ouro teve um desempenho impressionante, crescendo por

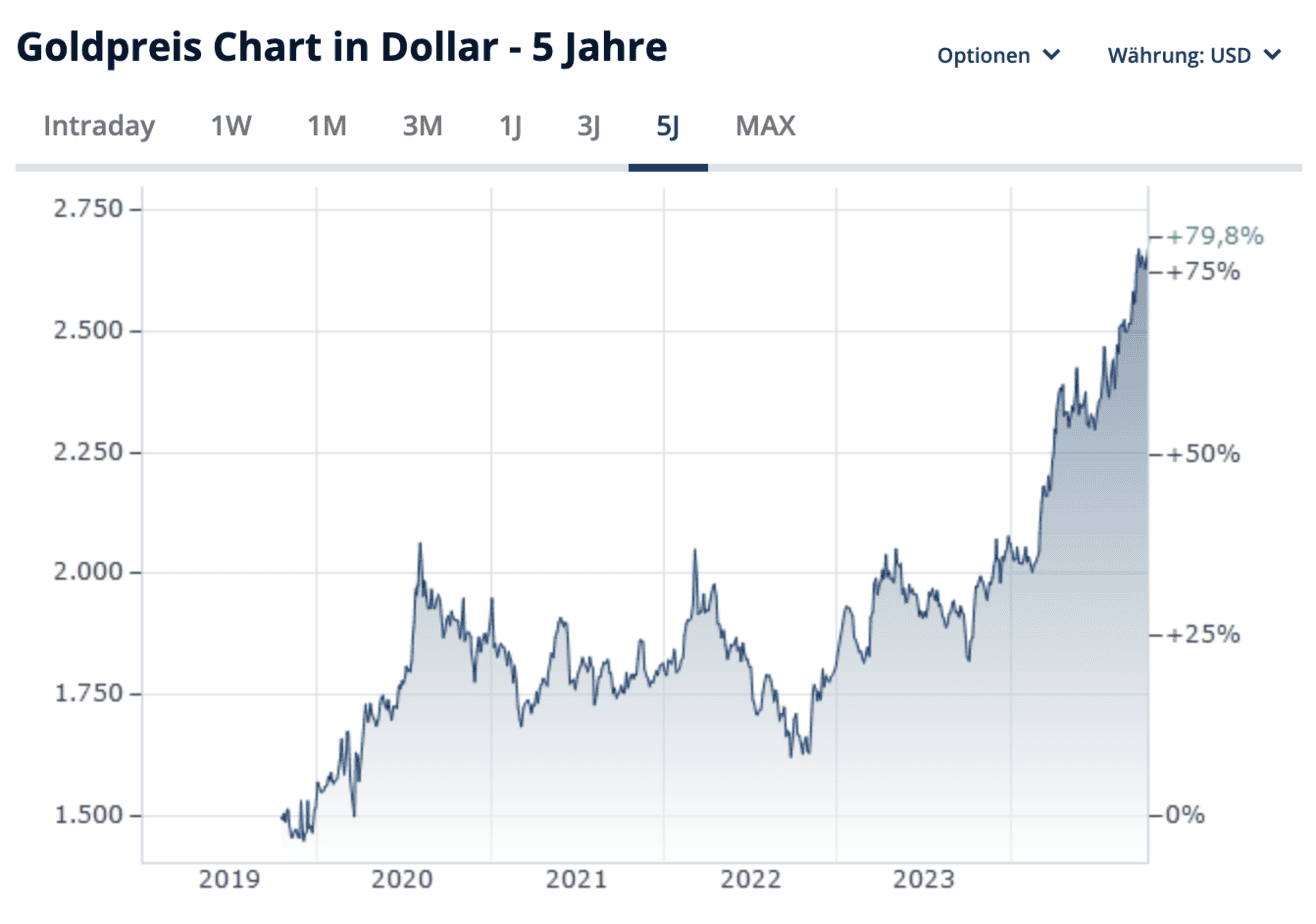

The Case for Gold and Precious Metals

Precious metals like gold and silver are often overlooked, but they can be a solid addition to a well-rounded investment portfolio. Over the past five years, gold has seen an impressive performance, growing by mais de 70% . Uma grande vantagem de investir em ouro é a capacidade de evitar o

While past performance doesn’t guarantee future results, gold has historically been a stable investment. One major advantage of investing in gold is the ability to avoid the 25% tax on profits if you hold it for at least a year . This makes it an attractive option for those looking to diversify their child’s portfolio and Hedge contra a volatilidade do mercado . Fundação

Conclusion

Investing for your child is not just about setting aside money—it’s about building a strong financial foundation para o seu futuro. Com apenas € 62 por mês e as estratégias de investimento corretas, você pode potencialmente transformar essa soma modesta em um milhão EUROS by the time your child retires, so that you can make your child a millionaire . Comece cedo, invista com sabedoria e seu filho agradecerá por configurá-los para o sucesso financeiro ao longo da vida. Para reservar uma reunião grátis conosco, use isso

The combination of government subsidies, tax savings , and smart investing will not only secure their financial future but also teach them valuable money habits . Start early, invest wisely, and your child will thank you for setting them up for life-long financial success. To book a free meeting with us, use this link . Salário

Pingback: How to Become a Millionaire in Germany on an Average Salary