A propriedade que compra o dilemma entre a Alemanha || 110 BIM BIME. 🤔 Você pode ler mais sobre isso neste artigo. Abordagem

In the world of real estate investment in Germany, the choice between small and big properties is a pivotal decision. 🤔 You can read more about this in this article.

Key Takeaways

- Property choice in Germany: Small or big property? Tailor your investment to match your personal strategy .

- David’s small property approach : Receita passiva segura, de baixo risco, real e menos alavancagem. renda. Considere a eficiência do fluxo de caixa. Consulte A

- Larry’s big property approach : High-risk, rapid wealth, fast acquisition, high leverage, income depends on earnings.

- Pros and Cons of David’s strategy: Safety, lower mortgage, after-tax passive income. Consider cash flow efficiency.

- Pros and Cons of Larry’s strategy: Risky, potential rapid wealth, quick acquisitions, liquidity support required.

- There is no universal answer . Consult with a Consultor financeiro para escolher com base em seus objetivos e status financeiro. Para acessar o conteúdo real, clique no botão abaixo. Observe que isso compartilhará dados com provedores de terceiros. Entre estes, um dilema se destaca com destaque: você se aventura no mercado

You are currently viewing a placeholder content from YouTube . To access the actual content, click the button below. Please note that doing so will share data with third-party providers.

More InformationIntroduction

Investing in properties in Germany presents a compelling opportunity , but it’s not without its pivotal decisions. Among these, one dilemma stands out prominently: Do you venture into the Mercado imobiliário com a Propriedade de investimento menor , sua propriedade para a propriedade Swift, ou você define seus miras em A || 161 larger property that enables you to leverage your investment to a greater extent? It’s a question that sparks extensive debate, and the answer is anything but universal. Your choice in this matter hinges on the intricacies of your personal investment strategy.

In this comprehensive guide, we delve into the heart of this real estate riddle, shedding light on the advantages and drawbacks of both investment approaches. By the time you reach the conclusion of this article, you’ll possess the knowledge required to make a well-informed decision, one that aligns with your Objetivos de investimento exclusivos . Quer você priorize a segurança e a estabilidade ou busca o potencial de acumulação de riqueza acelerada, o caminho que você escolher deve ser um reflexo de sua estratégia individual e aspirações financeiras. Vamos embarcar nessa jornada esclarecedora para o mundo de Investimento imobiliário Na Alemanha. Pado de campainha:

Small vs. Big Property Investment:

To help you better understand the property buying dilemma, let’s compare two hypothetical investors, David (The Downpayer) and Larry (The Leverager).

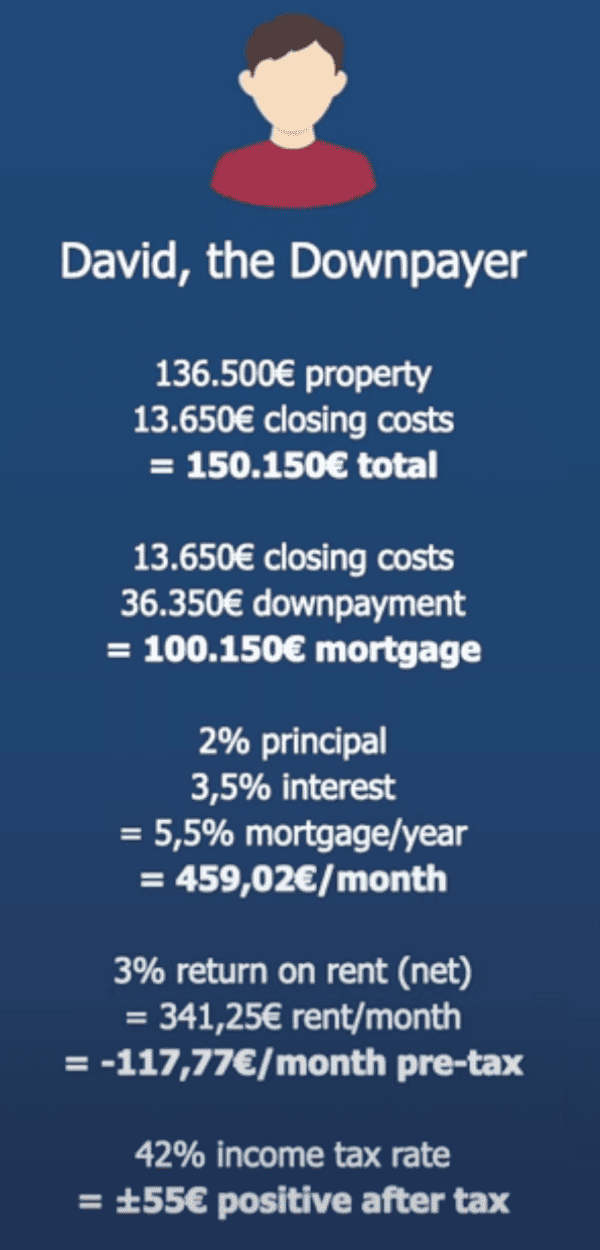

David - The Downpayer:

David possui 50.000 € Disponível para o seu Investimento imobiliário . Ele decide usar o seu 50.000 € como a Pagamento de adiantamento Ao comprar uma propriedade de aluguel. Com essa abordagem, ele compra a menor propriedade possível, ao preço de 136.500 € . A razão por trás dessa opção é a necessidade de alocar aproximadamente 10% para custos de fechamento, incluindo taxas de notário, Impostos e taxas de agente imobiliário. Sua inicial

In total, David’s investment amounts to just over 150,000€ . His initial 50.000 € serve como adiantamento, enquanto o restante 100.000 € são cobertos por A Mortgage . Este 100.000 € Mortgage representa o lowest amount banks typically find feasible. Mortgage rates generally remain high despite a down payment. This means that David’s mortgage rate is not significantly lower than if he had não fez um adiantamento. Neste exemplo, assumimos 3,5% . No entanto, seu fluxo de caixa antes dos impostos permanece ligeiramente

Assuming a 3% return on rent , David receives 4,000€ annually or 341€ per month after expenses. However, his pre-tax cash flow remains slightly negativo devido ao pagamento da hipoteca subtraído de sua receita de aluguel. Esse fluxo de caixa negativo se torna o mais benéfico de impostos possível quando a renda tributável de Davi exceder 63.000 € em 2023, como o Imposto de renda = Alavanca: 42% afterwards.

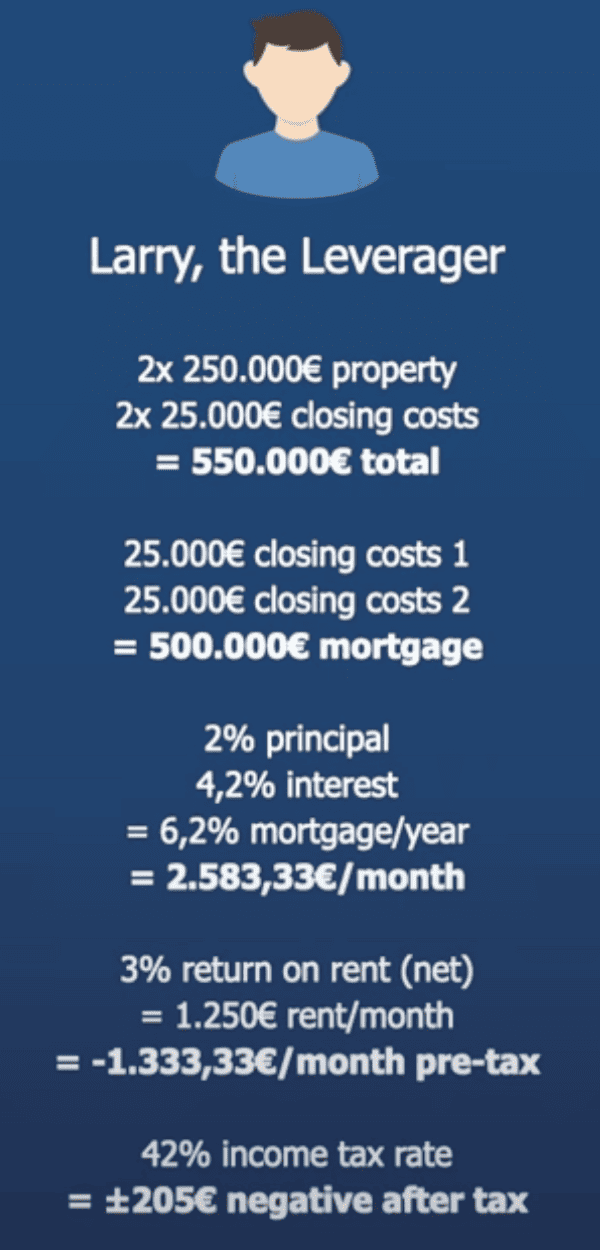

Larry - The Leverager:

Como David, Larry também possui 50.000 € para investir. No entanto, Larry adota uma abordagem diferente. Ele escolhe NOT para fazer um adiantamento e, em vez disso, ALVANHAS seu investimento com uma hipoteca bancária. Larry investe em dois Propriedades , cada um com preço 250.000 € , totalizando meio milhão de euros. Ele cobre o 50.000 € Custos de fechamento para ambas as propriedades, resultando em A Investimento 100% financiado . Vamos assumir um

Due to the lower downpayment amount, Larry’s mortgage rate is typically slightly higher than David’s. Let’s assume a 4,2% Taxa de juros. Isso se traduz em um pagamento mensal de hipoteca de quase 2.600 € . Receita de aluguel de Larry, em A 3% Retorno do aluguel , equivale a 1.250 € por mês, levando a um fluxo de caixa pré-imposto de aproximadamente || .. 254 -1,300€ monthly.

However, Larry benefits significantly from tax deductions devido aos seus juros hipotecários, depreciação e outras despesas dedutíveis de impostos. Com A 42% Taxa de imposto, Larry's Fluxo de caixa após impostos é cerca de 25 euros negativos por mês. vantagens e desvantagens de cada método. Ambas as abordagens têm seus méritos e limitações, tornando essencial alinhar sua escolha com suas circunstâncias financeiras e objetivos de investimento. Ao fazer um adiantamento substancial, ele reduz sua dependência do financiamento, minimizando sua exposição a flutuações das taxas de juros e incertezas econômicas. Essa abordagem é ideal para investidores que buscam estabilidade e segurança em seus investimentos.

Pros & Cons of Both Real Estate Investing Options:

When deciding between a small downpayment approach like David’s and a leveraging strategy like Larry’s, it’s crucial to consider the specific advantages and drawbacks of each method. Both approaches have their merits and limitations, making it essential to align your choice with your financial circumstances and investment objectives.

David's Downpayment Approach:

Pros of David’s Approach:

- Safe and Low-Risk Strategy: David’s downpayment approach is a conservative and low-risk strategy. By making a substantial downpayment, he reduces his reliance on financing, minimizing his exposure to interest rate fluctuations and economic uncertainties. This approach is ideal for investors seeking stability and security in their investments.

- Lower Leverage Means a Lower Monthly Mortgage Payment: Como o investimento de David depende menos de fundos emprestados, seu pagamento mensal de hipoteca é relativamente menor que o de Larry. Isso pode ser vantajoso para os investidores com fluxo de caixa mensal limitado ou aqueles que preferem um compromisso financeiro mais previsível. Ele pode desfrutar dos benefícios financeiros de seu investimento sem precisar cobrir um déficit mensal substancial. Além disso, as deduções fiscais das despesas podem melhorar ainda mais esse fluxo de caixa, fornecendo um fluxo constante de receita. Como ele está usando uma parcela significativa de seus fundos como adiantamento, ele pode perder os ganhos potenciais que a alavancagem pode oferecer. Ele pode achar desafiador diversificar e expandir seu portfólio imobiliário, que pode limitar seu crescimento financeiro geral. Essa estratégia é adequada para indivíduos com uma fonte de renda robusta e aqueles que estão confiantes em sua capacidade de sustentá -la. Os altos ganhos podem ajudar a compensar o fluxo de caixa negativo criado pela alavancagem. Com cada pagamento hipotecário, ele está efetivamente comprando uma parte de seu investimento, levando ao acúmulo de riqueza que pode superar as abordagens mais conservadoras. Isso pode resultar em investimentos diversificados, aumentado

- Real Passive Income on an After-Tax Basis: David’s strategy often leads to positive after-tax cash flow, meaning he’s generating real passive income . He can enjoy the financial benefits of his investment without having to cover a substantial monthly deficit. Moreover, tax deductions on expenses can further enhance this cash flow, providing a steady stream of income.

Cons of David’s Approach:

- Slower Wealth Accumulation: While David’s approach is safe, it may result in slower wealth accumulation compared to high-leverage strategies. Since he’s using a significant portion of his funds as a downpayment, he might miss out on the potential gains that leveraging can offer.

- Limited Investment Capacity: With his funds tied up in a single property, David’s investment capacity may be restricted. He might find it challenging to diversify and expand his real estate portfolio, which can limit his overall financial growth.

Larry's Leveraging Approach:

Pros of Larry’s Approach:

- High-Risk Strategy That Depends on High Earnings: Larry’s leveraging approach is considered high-risk and depends on the investor’s ability to generate high earnings. This strategy is suitable for individuals with a robust income source and those who are confident in their ability to sustain it. High earnings can help offset the negative cash flow created by leveraging.

- The Potential for Rapid Wealth Accumulation: Leveraging allows Larry to acquire multiple properties and build his real estate portfolio rapidly. With each mortgage payment, he’s effectively purchasing a part of his investment, leading to wealth accumulation that can outpace more conservative approaches.

- Fast Property Acquisition Due to High Leverage: Larry’s high-leverage strategy provides him with the flexibility to acquire multiple properties. This can result in diversified investments, increased Receita de aluguel e apreciação potencial de capital. É uma abordagem dinâmica para quem deseja aumentar seus ativos imobiliários rapidamente. A estratégia de Larry depende da manutenção de uma renda estável para cobrir o fluxo de caixa negativo e os pagamentos de hipotecas. Descunda econômica, mudanças nas taxas de juros ou perda de emprego podem representar riscos substanciais para essa abordagem. Isso significa que ele pode não desfrutar do mesmo nível de renda passiva que David, o quedas de junção. Em vez disso, seu foco está no acúmulo de riqueza a longo prazo, em vez da geração imediata de renda. Um aumento nas taxas de juros da hipoteca pode afetar significativamente suas despesas mensais e a estabilidade financeira geral. Este é um fator crucial a considerar em estratégias de alta alavancagem. Ajudaremos você a encontrar a melhor solução para você. Essa decisão crítica depende de suas circunstâncias financeiras, sua tolerância ao risco e suas metas específicas de investimento. Sua estratégia de baixo risco, alimentada por um adiantamento substancial, garante um compromisso mensal de hipoteca menor. É importante ressaltar que ele colhe renda passiva real em uma base após impostos, fornecendo

Cons of Larry’s Approach:

- High Risk and Volatility: Leveraging comes with a significantly higher level of risk and volatility. Larry’s strategy depends on maintaining a stable income to cover negative cash flow and mortgage payments. Economic downturns, changes in interest rates, or job loss can pose substantial risks to this approach.

- Limited Passive Income at the Outset: Larry’s leveraging approach often results in negative cash flow initially. This means that he may not enjoy the same level of passive income as David the downpayer. Instead, his focus is on long-term wealth accumulation rather than immediate income generation.

- Exposure to Interest Rate Fluctuations: Larry’s approach leaves him exposed to interest rate fluctuations. An increase in mortgage interest rates can significantly impact his monthly expenses and overall financial stability. This is a crucial factor to consider in high-leverage strategies.

Conclusion

In the realm of German real estate investment, the choice between a small, swiftly paid-off property and a larger, highly leveraged investment is not a matter of right or wrong but of personal strategy . This critical decision ultimately hinges on your financial circumstances, your risk tolerance, and your specific investment goals.

David’s method is a testament to safety and prudence . His low-risk strategy, powered by a substantial down payment, ensures a lower monthly mortgage commitment. Importantly, he reaps real passive income on an after-tax basis, providing Estabilidade financeira . É um método caracterizado por uma sede de acumulação rápida de riqueza. Sua alavancagem pesada

Larry’s approach is high-stakes, relying on the potential for robust earnings . It’s a method characterized by a thirst for swift wealth accumulation. His leverage-heavy Estilo de investimento Permite a rápida aquisição de propriedades, finalmente promovendo crescimento financeiro . A escolha certa depende do seu

As you weigh these approaches, remember there’s no definitive answer to the small vs. big/many property investment debate. The right choice depends on your Situação financeira e metas de investimento . Os investidores com segurança podem gravitar em direção à abordagem de pagamento de David, enquanto aqueles com apetite de alto risco e ganhos substanciais podem favorecer a abordagem de alavancagem de Larry. Escolha sabiamente e embarcar sua jornada de investimento imobiliário com confiança, sabendo que você adaptou sua estratégia para se adequar às suas aspirações e circunstâncias únicas.

The German real estate market offers diverse opportunities, but it’s your strategic approach that will ultimately determine your success . Choose wisely and embark on your real estate investment journey with confidence, knowing that you’ve tailored your strategy to suit your unique aspirations and circumstances.

Pingback: Construindo sua própria empresa imobiliária (GmbH) na Alemanha do Scratch

Pingback: 5 maneiras acessíveis de investir no setor imobiliário na Alemanha || Investimento?

Pingback: Is Real Estate In Europe A Bad Investment?

Pingback: Top 5 erros ao comprar uma propriedade na Alemanha